Most entrepreneurs start organizations because they are passionate about the primary work of the business – which usually isn’t accounting. This means that most entrepreneurs aren’t completely comfortable interpreting the monthly financial reports they receive.

All Profit & Loss Reports, or P&L’s, are based on a very simple formula…Sales minus Costs equals Profit. It really is that simple.

Everything else is a matter of breaking out sales or cost into more detail and adding subtotals. Sales (or ‘revenue’ or ‘income’) are typically shown at the top of the P&L. Costs (or expenses) are shown below sales and profit is at the bottom. You may see a number of subtotals as you look down the column, but it is still: sales – costs = profit.

Sales may be broken into several different sources. For example, the sales of a restaurant may come from customers who dine in or take out or from catering

Similarly, costs are usually broken into various components. For example, you may see material costs, labour costs and overhead broken out separately.

Cost directly relating to products purchased for the sole purpose of making the goods you sell; are referred to as cost of goods sold (COGS) because they can be tied directly to the production of your item.

If you have been filing your P&Ls away without reading them, you are not alone. However, understanding your P&L is essential to being able to run your business successfully.

Remember always view your Profit & Loss Reports, and other reports, in the Accounting method your business is using – Cash or Accrual (See Difference between Cash and Accrual Accounting Sheet)

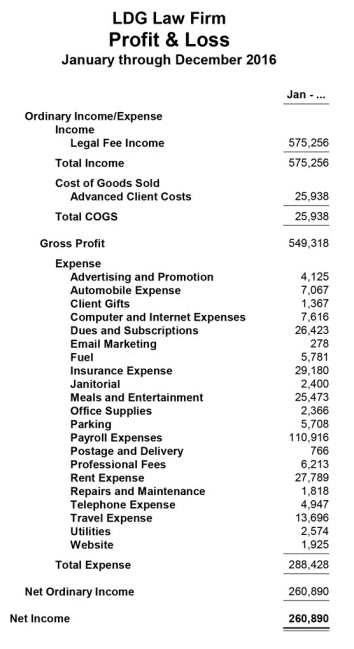

A Sample Profit & Loss report: